International Trade Week Reflections on a shifting landscape

With International Trade Week comes much opportunity to reflect on the world of trade, which, I think it’s safe to say, has had quite the bumpy ride over the last few years.

International trading conditions have shifted into an environment that doesn’t necessarily scream ‘welcome’ to firms looking for growth. It is a world that, particularly in the past year, has been shaped by tariffs and sanctions and greater levels of protectionism, a movement that indicates a retreat from a system of free and open trade.

Even before the US administration sent ripples through the global order by provoking escalation of such trade controls, a combination of the Covid-19 pandemic, Russia’s invasion of Ukraine, China’s posturing over Taiwan, and the UK’s decision to leave the EU have intensified geopolitical pressures and revealed the fragility of global supply chains.

As a result, UK firms have suffered an increase in trade barriers, and the UK economy has suffered a decline in exports, threatening the UK’s competitiveness on the global stage. World Trade Organisation (WTO) figures show UK that trade performance has weakened since the 2008 financial crash, with Brexit being one of the primary contributors. According to the WTO, UK exports of goods languish at 17% below their pre-Covid levels, meanwhile out of 36 OECD countries, the UK ranks 31st or trade openness (typically defined as exports + imports as a % of GDP).

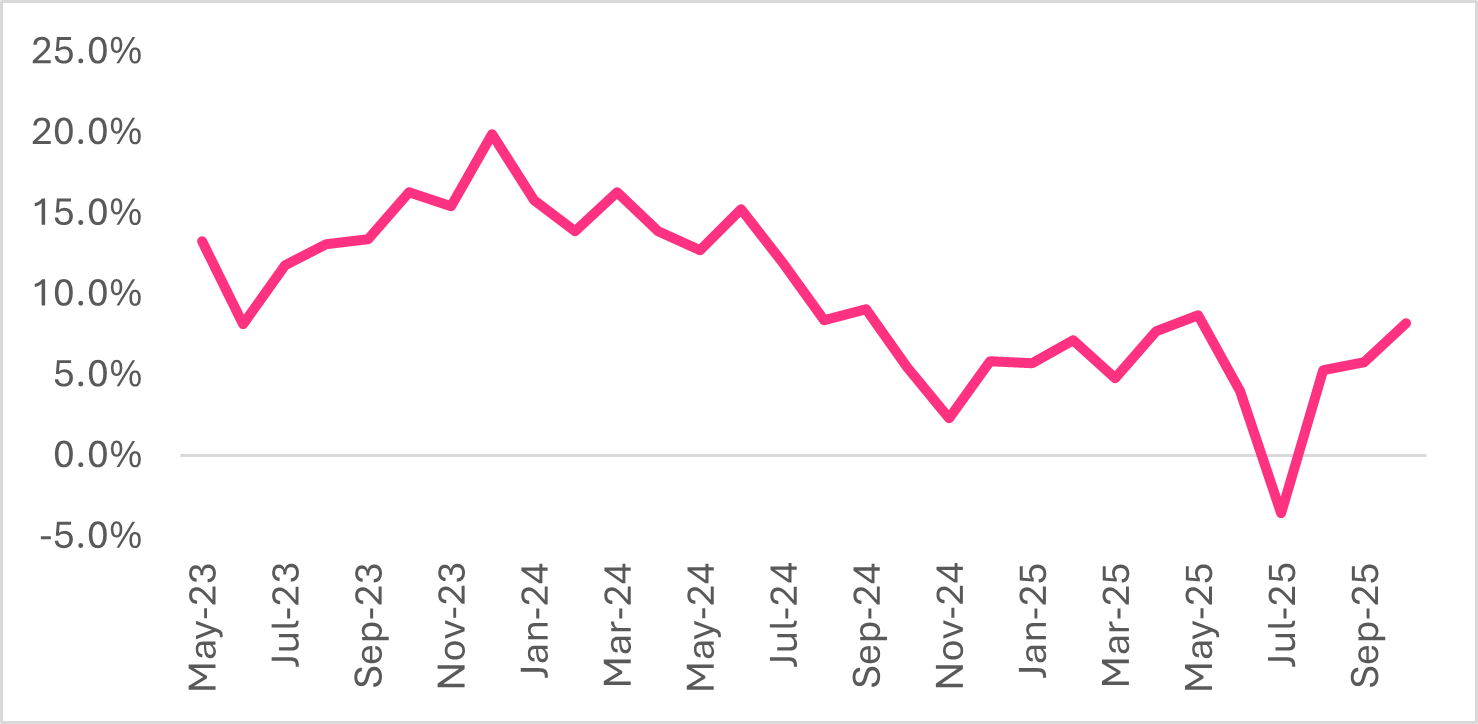

The IoD’s data shows business leader confidence in the prospects for exports over the coming 12 months has been more subdued in 2025 than it was in 2024.

Comparing the next 12 months with the last 12 months, what do you believe the outlook for your organisation will be in terms of exports:

Meanwhile, our data from June shows that almost 40% still experience barriers to trading with the EU, primarily paperwork (66%); time taken for checks at the border (41%); customs duties (41%); EU regulations e.g. REACH/GPSR (36%). 70% of members feel the UK’s relationship with the US is important to their organisation’s international strategy, but just a quarter are confident that the UK and US will sign a deal to build on the Economic Prosperity Deal negotiated in May this year.

Moreover, there is the deeper mindset issue amongst UK firms, especially amongst the smaller end of the scale, that exporting isn’t relevant to them, that they are too small and lack resource, and that they have sufficient demand in the UK already. In fact, only 11.9% of the UK’s business population currently exports. IoD data, that assesses the reasons why firms do not currently export but could, shows the top five reasons to be:

(IoD Policy Voice, January 2025)

On a more positive note, the government’s approach of balancing all trading partners equally has been welcomed by members. Additionally, the government’s Trade Strategy, published this summer, was possibly the most well received of the series of growth strategies. The hattrick deals the government negotiated this year with the US, the EU and India are viewed as positive achievements. Though on balance, for those that wish for the government to align more closely with one particular trading partner, the EU wins out by a significant margin:

The government has taken the approach of maintaining good relations with all of the UK’s trading partners. Do you believe that they should move to align more closely with the US or the EU?

(IoD Policy Voice, April 2025)

In practice, despite this good will, there is evidence of a discrepancy between the perception of the trade deals and the actual benefits they will bring to individual firms. For example, whilst members think the US and India deals – 47% and 60% respectively – are good for the UK, the vast majority think they will provide no benefits for their own organisations: US (69%); India (70%).

Understandably, the US is perceived to be an unstable trading partner in light of the tariff agenda and related trade wars:

“It’s the “don’t know” that is the most damaging. The US is our biggest market and investment in capital equipment by our customers there has slowed significantly, because they don’t know what’s coming either.” (South East England, Manufacturing, 250+ employees)

“The Trump administration has proved itself to be utterly untrustworthy, so any trade deal is either unlikely to be beneficial for the UK or, if it is, the US Government will renege on the terms.” (Scotland, Professional, scientific and technical activities, 2-9 employees)

“UK/US relationship shapes so much of whatever we all do. The mercurial nature of US policy unfortunately makes ‘doubt and uncertainty’ the norm.” (Scotland, Other services, 2-9 employees)

There is a minority of firms that are looking to the US as a higher growth industry that will offer the UK many more opportunities:

“The AUKUS agreement is key for many areas of technology cooperation and linked sales opportunities. These must be leveraged to sales in the UK, Australia and 3rd countries. The US market, as a whole, is more vibrant and successful than the slow, bureaucratic EU. If we want growth it will come if we align with fast growing, entrepreneurial markets such as US and CPTPP.” (South West England, Manufacturing, 250+ employees)

“Growth and free trade are more likely via US than EU collaboration.” Wales, Financial Services, 10-49 employees)

“The UK would far much better trading with the USA if UK Government policies were more aligned with the USA – low energy prices, low tax, pro growth and this would be the best help of all for UK PLC and trade with the USA – sadly it seems we will have to wait for the next Gov before this can happen.” (West Midlands, Information and communication, 100-249 employees)

Ultimately, members see the EU as the UK’s most reliable partner. Nevertheless, there is still a long way to go to progress on the UK’s reset of relations with the EU as details are hashed out over a Sanitary and Phytosanitary agreement and a Youth Mobility Scheme, and it is unclear, despite significant political thawing, how eager Brussels is to continue to make an example of the UK’s Brexit decision:

“The EU is our largest market and trading partner and we shot ourselves in the foot with Brexit. We should seek to correct much of this self inflicted damage and work to reforge positive working and trading relationships with Europe.” (South East England, Professional, scientific and technical activities, 2-9 employees)

“If the US want to be isolationist in their approaches to world trade then so be it. We should trade wrap ourselves with very much the EU markets in mind. However, as we all know Brexit has done more harm than good, so this has to be a long term strategy.” (East Midlands, Manufacturing, 100-249 employees)

“The US has become a basket case, being on a rogue nation, and cannot be trusted on anything. The EU has been consistently reliable, open and dependable.” (East Midlands, Financial services, 2-9 employees)

All this marks a pivotal moment for UK trade. Businesses are navigating an increasingly complex international trading environment, marked by uncertainty and evolving geopolitical relations. Firms are having to be much more adaptable in their international strategies, with many looking to move away from certain ‘risky’ markets, or to shift their supply chains to countries perceived to be more reliable friends of the UK. Meanwhile, the good optics that accompany trade deals are not worth much if firms don’t feel they can grasp the opportunities. The challenge remains how best to ensure the benefits of the UK’s trade agreements reach firms of all sizes and at all stages of their export journeys.

It was a pleasure to have been able to dig into these reflections with a brilliant panel of experts, Michael Martins, Sarah Edwards MP and Jill Rutter, at an event hosted by Overton Advisory on how global shifts are reshaping business, diplomacy and policy. We did our best to put the world to rights. And for further analysis from the IoD on how the UK’s trading performance can be improved, do have a look through our Budget Submission here.

About the author

Emma leads on the IoD’s policy work on international trade and EU affairs. She works with UK businesses, trade bodies and the government to advocate on behalf of IoD members on issues relating to the UK’s trading relationship with the EU, Free Trade Agreements, supply chain disruption and geopolitics.

Brexit 10 years on

Read Emma Rowland’s in-depth analysis of the UK-EU relationship – including additional survey data and feedback from IoD members about Brexit’s impact – here.

Join a thriving community of skilled directors and leaders

Ask us about membership