Brexit 10 years on

An hour is a long time in British politics at the current rate of the game. 10 years is a different story. A massively long and complex one. Once upon a time, this day a decade ago, I was halfway through sixth form college in the midst of sitting my AS Levels. I was not even old enough to vote, something that has given me a useful ‘out’ whenever I have been asked whether I belong to the 52% or the 48%. But even underage, and removed as I was from the Whitehall bubble, the polarising emotion that defined the Brexit debate was overwhelming.

At the centre of the Remain campaign was the warning of economic risk and trade shock that a UK shoved outside of the Customs Union and Single Market would face. The ‘Out’ tent was focused on sovereignty and immigration. Their rebuttal to the remainers’ economic concerns was that the UK sent £350 million a week to EU, a sum that could be better spent on domestic priorities. Running through these economic arguments was the question of where the UK’s cultural, social and historical identity and belonging really lay. No-one really knew what the real impact would be, which was why so much of the campaigns hinged on voter emotion – for the remainers, Project Fear; for the leavers, ‘take back control’.

Now, much of my work life is spent looking at the business implications of the UK’s trading relationship with the EU. The policy and economics remain complicated. The politics remains sensitive. It was a bad breakup, and it is possibly an even messier reconciliation.

A withdrawal agreement, a Trade and Cooperation Agreement (TCA), a Northern Ireland Protocol, a Windsor Framework and 5 Prime Ministers later, it’s the now former Prime Minister Sir Keir Starmer who has made the most progress towards a ‘Reset’ of sorts. It’s progress of the ‘work in’ variety.

The TCA now governs the UK’s trading relationship with the EU. On 30 December 2020, the UK Government and EU concluded negotiations for the TCA, to dictate their future relationship, based on three primary themes: trade, cooperation, and governance. The agreement came into force provisionally on 1 January 2021, and was approved for ratification by the EU Parliament that April.

The TCA ensures zero tariffs or quotas on trade across the border where goods meet the relevant rules of origin. This means that goods have to have been processed sufficiently within the UK or EU to qualify for liberalised market access. The TCA also allows for both sides of the Channel to regulate goods in the way most appropriate for their own market, and maintain their own customs processes to protect their respective regulatory, security and financial interests.

Meanwhile, services trade is based on WTO commitments. The UK and EU agreed not to impose restrictions for short term business visitors, allowing business visitors to travel to the EU for 90 days in any 180-day period.

Endless paperwork

Interestingly, the view on the ground in the EU is that the TCA is a comprehensive, modern trade agreement – one of their best. The view on the UK side of the sea isn’t quite so optimistic. The thing is, UK exporters continue to face friction at the border, particularly relating to customs and business mobility.

A survey we conducted with 449 members in June 2025 found that 39% of members experience barriers to trade with the EU. If we only focus on those who actually do trade with the EU, that proportion rises to 61%.

To what extent does your organisation experience barriers to trading with the EU?

Of these, paperwork (66%), the time taken for checks at the border (41%) and customs duties (41%) were the biggest barriers. A quarter cited restrictions on business travel as a challenge.

Our members describe the issues best:

Becoming accustomed

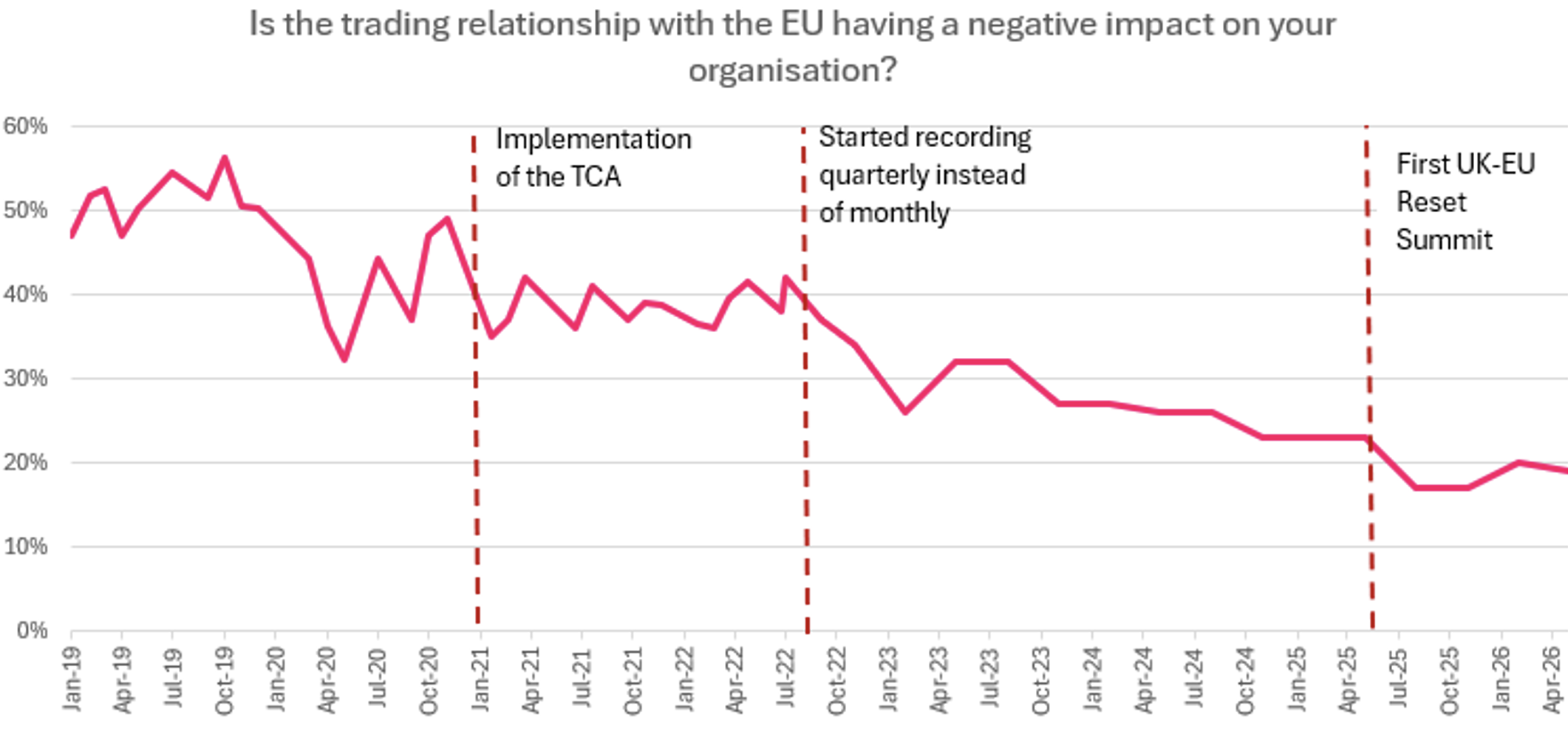

These challenges present very real everyday friction for UK exporters. That being said, IoD data shows that the organisational impact of the UK’s trading relationship with the EU has softened over time, falling down the list of concerns. The IoD tracks factors that are having a negative impact on members’ organisations on a quarterly basis. Over the last few months, the consistent top 5 factors have included UK economic conditions, employment taxes, business taxes, global economic conditions, and the cost of energy. For the first time since the question was initially asked in January 2019, ‘the UK’s trading relationship with the EU’ dropped out of the top 5 in November 2023.

Anecdotally, contributing factors to this easing of sentiment include the fact that members are just getting used to the new arrangements – less of the unknown. On the other hand, there are those firms for which cross-Channel trade was simply too difficult that have now ceased trading with the EU, and so the trading relationship has become no longer relevant. Meanwhile the narrative has shifted slightly as coverage has focused on the importance of the government’s Reset programme, and noise around progress of different commitments, such as on Sanitary and Phytosanitary (SPS) arrangements (regulatory measures on human, animal and plant health), emissions trading and electricity trading, have built confidence.

And of course, as external events, such as the implementation of tariffs, or a regional conflict in the Middle East, or the cost of energy, or the labour market crisis have increased in importance, the perception of the challenge of the EU may have dampened.

The wider context is important to note here as well. International trading conditions have shifted into an environment that doesn’t necessarily scream ‘welcome’ to firms looking for growth. It is a world that, particularly in the past couple of years, has been shaped by tariffs and sanctions and greater levels of protectionism, a movement that indicates a retreat from a system of free and open trade.

Even before the US administration sent ripples through the global order by provoking escalation of such trade controls, a combination of the Covid-19 pandemic, Russia’s invasion of Ukraine, China’s posturing over Taiwan, and indeed Brexit itself, have intensified geopolitical pressures and revealed the fragility of global supply chains.

The Reset

As a result, the gravitational pull towards the EU has strengthened markedly, both for the UK government and for UK businesses. New research that we have published reveals this shift in business sentiment, with 52% of business leaders believing the government should now make the EU its top trading priority. This represents a significant increase from 35% in April 2025, underlining growing recognition of the EU’s importance to UK business.

The government has taken the approach of maintaining good relations with all of the UK’s trading partners. However, more recently, it has signalled it will be pursuing closer alignment with the EU. Which of the following do you agree with the most? (April 2026)

In contrast, the proportion of respondents who believe the government should approach all trading partners equally has fallen to 35%, down from 41%. Support for prioritising the US has dropped sharply, with just 2% of business leaders identifying it as the top priority, compared to 10% last year. The shift away from transatlantic trade is symptomatic of this strive for predictability, something that the US is not offering at the moment.

So, businesses are very much welcoming the government’s focus on resetting relations with the EU. The first UK-EU Reset Summit took place on 19 May 2025, and introduced a ‘Common Understanding’ that “sets out the conclusions of those exploratory talks”. These include the negotiation of an SPS agreement to remove swathes of border checks, such as health certificates and safety checks, on animal, plant and agrifood products; the linkage of respective Emission Trading Systems to provide a level playing field between carbon markets; and exploring UK participation in the EU’s internal electricity market. The two sides also committed to holding dedicated dialogues on short term business mobility and the recognition of professional qualifications to create a forum to address mobility barriers faced by UK services providers in the EU.

The economic impact of the announcements so far is a little hard to gauge. Starmer has said the deal would boost the economy by £9 billion a year by 2040. But most analysis finds that this isn’t nearly as much as the UK economy was hit due to Brexit. The Office for Budget Responsibility hasn’t changed its forecast that the economic impact of Brexit will hit UK GDP by 4% in the long run. There is also new data from the Bank of England that suggests Brexit has taken a 6% chunk out of the UK economy. This is based on internal Bank of England data about the decisions, views and financial results of thousands of British companies since the referendum a decade ago.

One of the only significant quantifiable impacts so far would be the veterinary deal, which could see agrifood exports to the EU boosted by more than 20% if there were to be high-alignment of regulation.

Of course, not everyone agrees that the nature of the Reset is the best course. Some members, anecdotally, feel that the EU’s machinery is so bureaucratic that it will actually stunt UK growth prospects:

Some feel there are areas where EU regulation risk stifling competition and innovation, meaning it would be more harmful for business and the UK economy to align. This is particularly felt in relation to AI and tech: while there is a strong imperative for closer alignment on AI research and governance, and AI research is primarily dominated by the US and China, there is concern that the EU AI Act is too restrictive to be beneficial for business, strongly prioritising safety over creating space for innovation.

The EU is embarking on its own programme to address regulatory barriers and slow growth. The Draghi Report, written in 2024 by the former Italian Prime Minister, Mario Draghi, proposes measures to close the innovation gap with the US, harmonise decarbonisation with competitiveness and enhance economic security by reducing dependencies.

In fact, Draghi estimates that it takes on average 19 months to pass a piece of legislation into law, depending on the complexity. Under the UK process, again depending on the nature of the Bill, it could take between 3-12 months to pass a piece of legislation through the UK parliament.

What now?

This is the most important question, not least given the Prime Minister’s resignation announcement yesterday (22 June). The second iteration of the UK-EU Summit is due to take place on 22 July, and will consolidate the progress already made on SPS, emissions trading and electricity trading. We are also expecting some movements on youth mobility negotiations, something that has consistently been a thorn in the reset side, and something that the IoD has been calling on the two sides to knuckle down and agree on…

There is also the incoming European Partnership Bill, announced in May at the King’s Speech, that will allow the UK to implement ‘dynamic alignment’ with certain areas of the EU’s regulation. It will firstly allow for the establishment of the agreements negotiated as part of the first reset summit, as stated above. It could also allow for closer alignment in other areas of regulation, thus addressing some of the administrative friction firms face at the border. Yet there are some potential issues to be worked through. Chief among them is ensuring that any regulatory changes serve the interests of UK businesses, first and foremost. The government’s explainer notes on the King’s Speech state that the UK will retain decision-making powers, but the devil will be in the detail.

But of course this is all continent on the UK’s latest leadership saga. We might expect the Summit to be rescheduled until a time when a new UK Cabinet has settled in. Meanwhile, we will be watching to determine the fate of the proposed European Partnership Bill. UK political instability has been on the list of EU concerns – particularly in the sense of what happens in the scenario that we end up with a government, e.g. Reform UK, that wants to unravel all progress and links with the EU Reset. But even on the left of the political spectrum, with the success of Andy Burnham in Makerfield last week, who is now likely moving to set up shop in Downing Street imminently, there lies the prospect of a new strategy altogether.

Burnham was coy throughout the Makerfield by-election campaign period on his line on the EU. Afterall, he was trying to win over a ‘leaver’ constituency. But he has historically been pro-rejoin.

The prospect of rejoining is not a particularly realistic one right now. Even if the UK did apply to rejoin the block, the EU-lite-esque terms we enjoyed as a member would be a tall order – opting out of the Euro, Schengen Zone, the UK Rebate, which was a policy Margaret Thatcher negotiated whereby the UK would get back 66% of the difference between what the UK contributed and what it received in EU funding.

On the one hand, former President of the EU Commission (2014-2019), Jean-Claude Juncker, reckons that we would be given the cold shoulder: “I don’t think [rejoining] is possible. Because all of us, we are wounded to some extent by this… historic step the British have taken”. He also highlighted the UK’s relationship with the US, which is not looked upon favourably by the EU in current times.

On the other, Michel Barnier, the EU’s Chief Brexit negotiator between 2016 – 2021, told the Guardian that he would see no problem with the UK re-entering with its special terms as before.

Meanwhile, public attitude 10 years on has shifted slightly. According to a YouGov poll, most Britons think the UK was wrong to leave the EU, including 23% of Leave voters. But only 55% say they would support the UK rejoining the EU, which falls to 35% if the UK had to join without its prior opt-outs.

The overall message from business is that we need a better working relationship with the EU and, as the global context stands, this should be the government’s top priority. The UK’s trading relationship with the EU is far from simple, and remains a brake on UK growth. But alongside this, there needs to be a sense of long-termism that underpins the government’s trade strategy. What does it want the UK-EU relationship to look like in another ten years’ time? The world may be enjoying a more stable and outward looking US President by then. Global conflicts might have eased. What happens if the EU is still suffering sluggish growth itself? Questions to be answered next decade, but that will shape the UK’s stance in the years to come…

About the author

Emma leads on the IoD’s policy work on international trade and EU affairs. She works with UK businesses, trade bodies and the government to advocate on behalf of IoD members on issues relating to the UK’s trading relationship with the EU, Free Trade Agreements, supply chain disruption and geopolitics.

Brexit 10 years on

Read Emma Rowland’s in-depth analysis of the UK-EU relationship – including additional survey data and feedback from IoD members about Brexit’s impact – here.

Join a thriving community of skilled directors and leaders

Ask us about membership