The Budget unpacked Growth strategy pending

After a messy build-up, the Budget landed in chaos on the 26 November with the Office for Budget Responsibility (OBR) mistakenly leaking its own report.

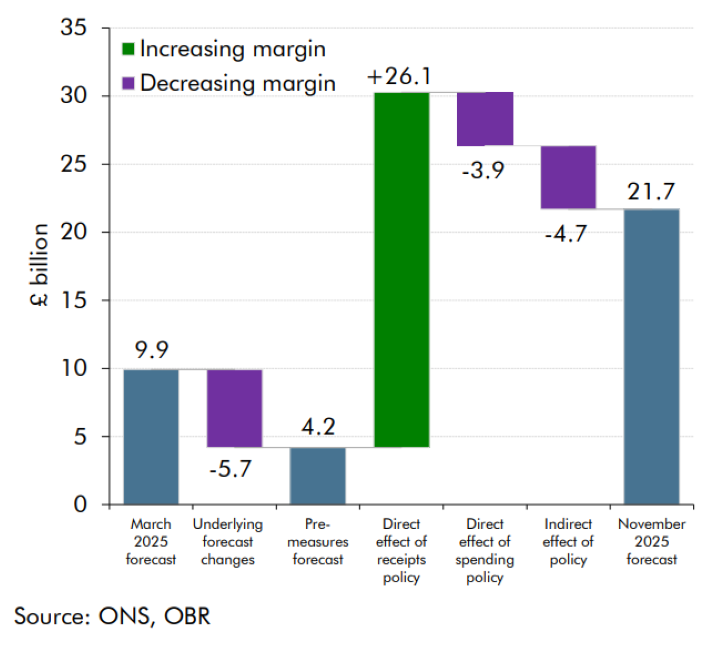

Perhaps the most astounding takeaway was that, after all the fuss over the potential size of the fiscal hole, there wasn’t one. The much anticipated productivity revisions were almost entirely offset by higher tax revenues due to inflation, enabling the fiscal rules to be met by a slimmer margin of £4 billion before policy decisions. And yet this Budget contained another £26 billion of tax increases following last year’s £41 billion. This year’s windfall goes to build more headroom against the fiscal rules (an extra £11 billion) in an attempt to enhance policy stability, to pay for summer welfare and fuel tax reversals (£7 billion) and the abolition of the two-child benefit cap (£3 billion). Borrowing increases too by £5 billion on average over the next three years. Meanwhile, it turns out that last year’s Budget, despite the economically damaging rise in employer NI, was actually better for growth than this year’s due to the increase in public sector capital spending that it delivered. In contrast, the OBR’s judgement is that nothing in this Budget materially changes it’s now downgraded growth outlook. This Budget loosens policy in the first three years, before it tightens sharply thereafter, with big rises in the tax take from 2029-30. So, austerity is once again pushed back.

The change in the current budget margin (first fiscal rule)

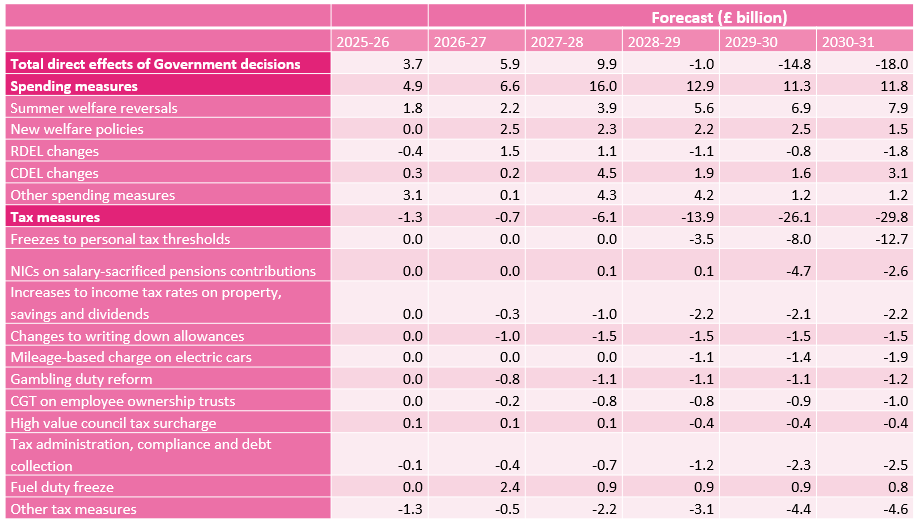

The policy detail

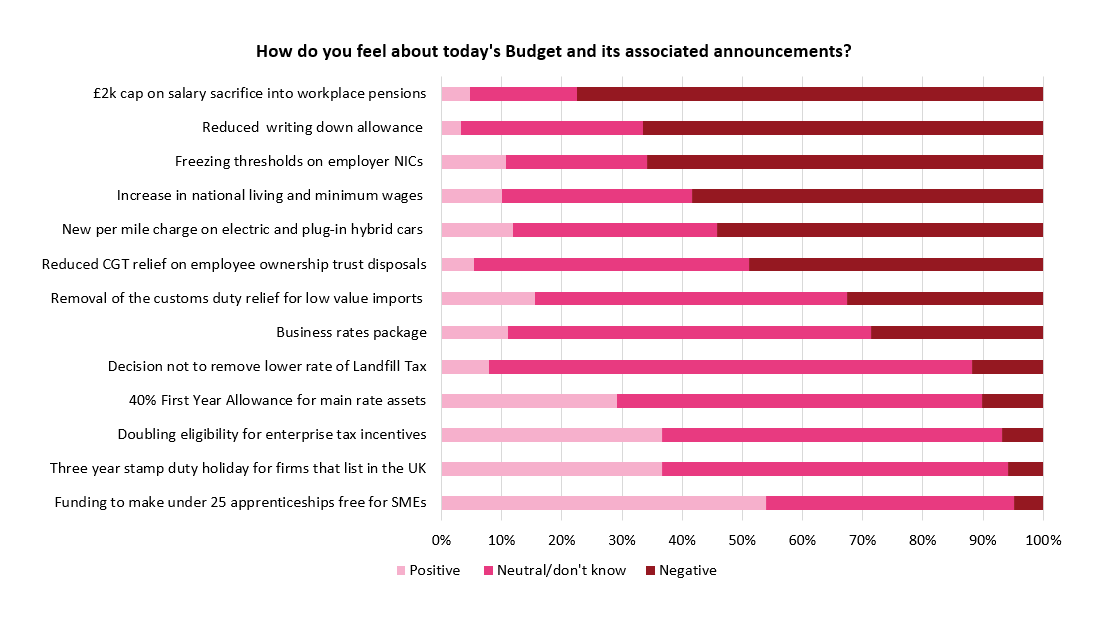

The business response to the Budget

Unsurprisingly, IoD members reacted negatively to a Budget which further increased their costs, particularly for employment. 80% felt more negative after the Budget, with the most negative sentiment surrounding the £2k cap on pension contributions eligible for NI relief, the cut to the main rate writing down allowance and the freeze in employer NIC thresholds. Combined these measures are seen to reduce investment incentives and increase employment costs. Set against that, the funding of apprenticeships for SMEs, doubling of the eligibility for enterprise tax incentives and the 40% first year allowance were judged positive, but members felt they were too narrow when set against cost increases elsewhere.

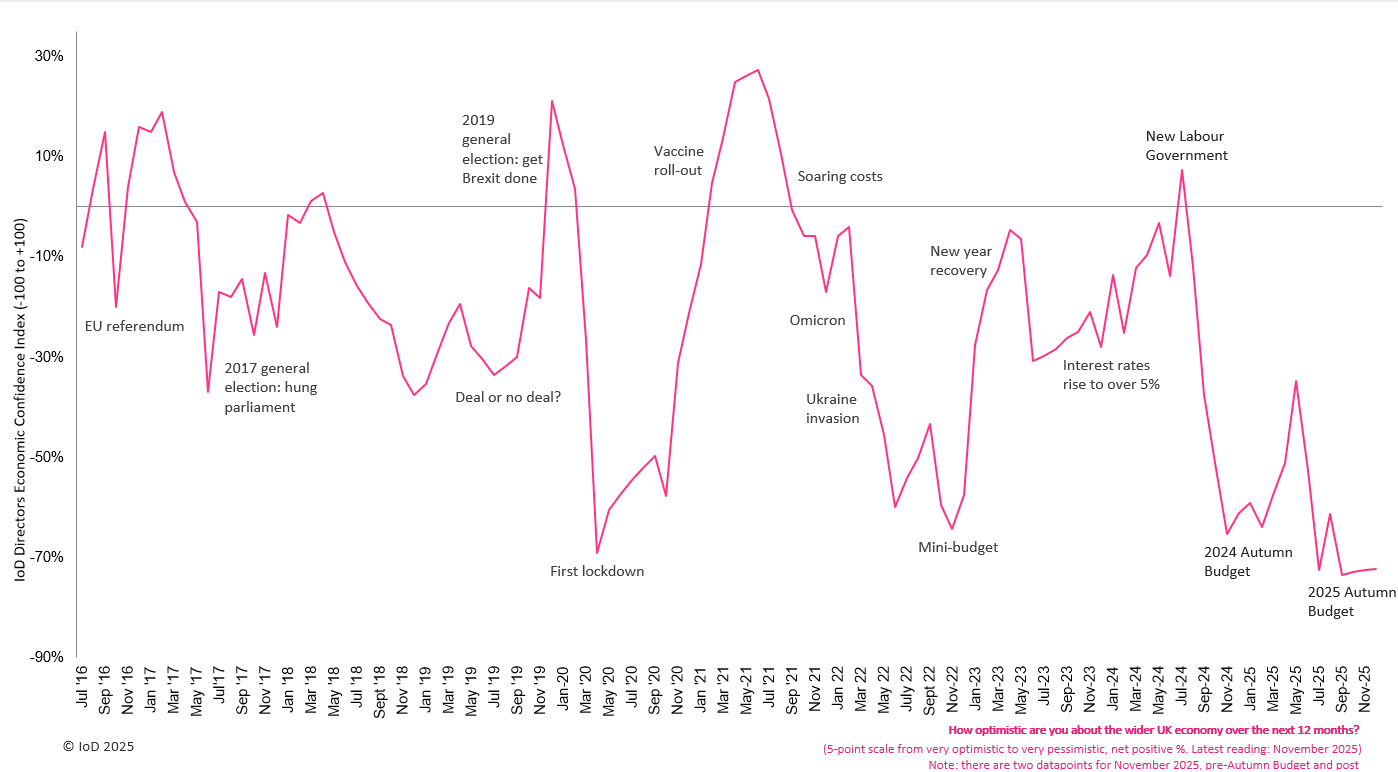

We ran our regular questions on directors’ confidence both before and after the Budget so that we could compare responses. The Budget led to little change in the rock bottom confidence of business leaders overall. More worryingly though were the downward moves in the economic time series.

- Revenue expectations fell to -8 (post-Budget), from +7 (pre-Budget) – the lowest since September 2020.

- Headcount expectations fell to -29, from -8. This is the indicator’s third lowest reading.

- Investment intentions fell to -39, from -17. This is the second lowest reading of this indicator, after May 2020 (-43).

These moves bode ill for an improvement in private sector activity – particularly for a recovery in investment which is urgently needed to lift productivity and living standards.

Growth and the public finances

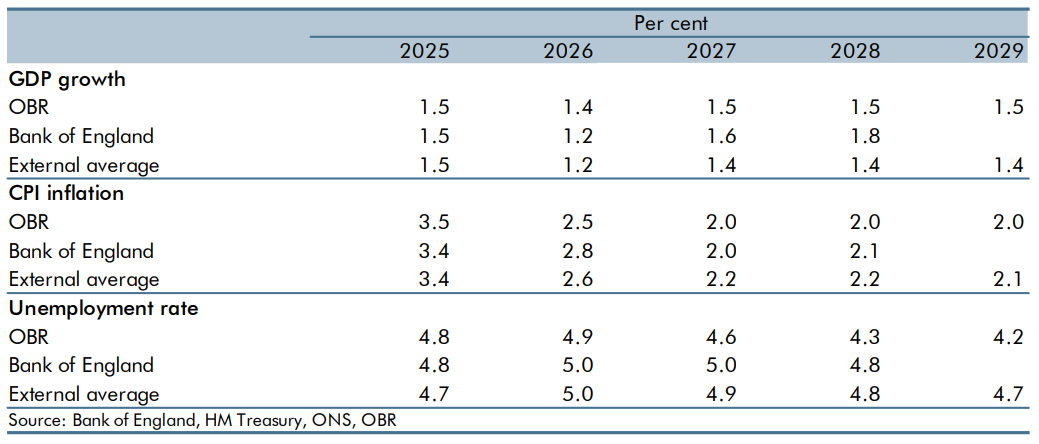

The OBR did ultimately deliver the expected downgrade to its productivity forecast. GDP is now expected to growth by 1.5% on average over the forecast period, 0.3% points lower than projected in March. Yet this didn’t hit the public finances as hard as expected. As has happened in the past, inflation came to the rescue, as did stronger wage growth relative to profits, delivering a boost to tax receipts. This was offset by higher public spending due to higher disability caseloads, higher debt spending and higher local authority spending on special educational needs and disabilities (SEND).

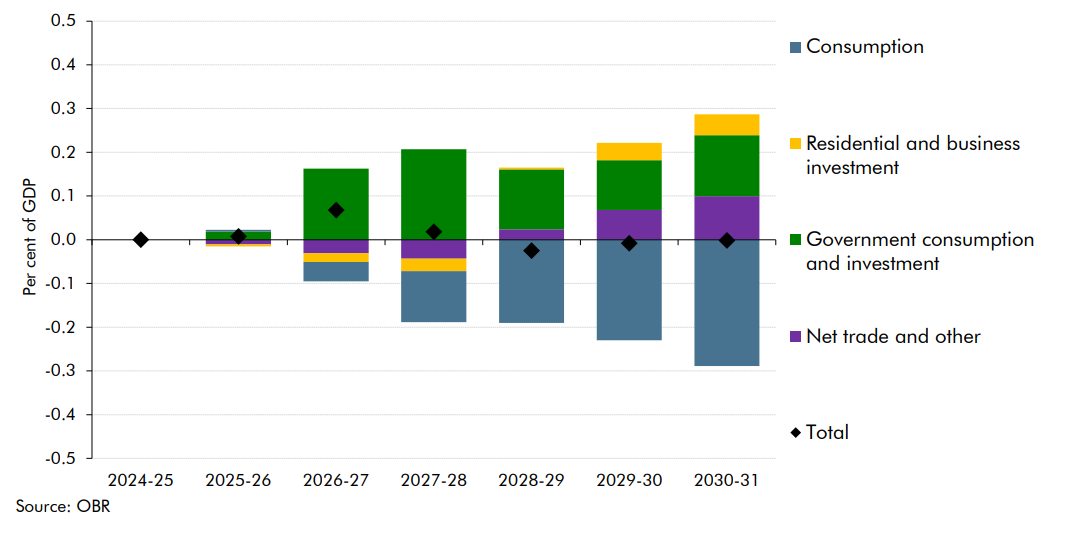

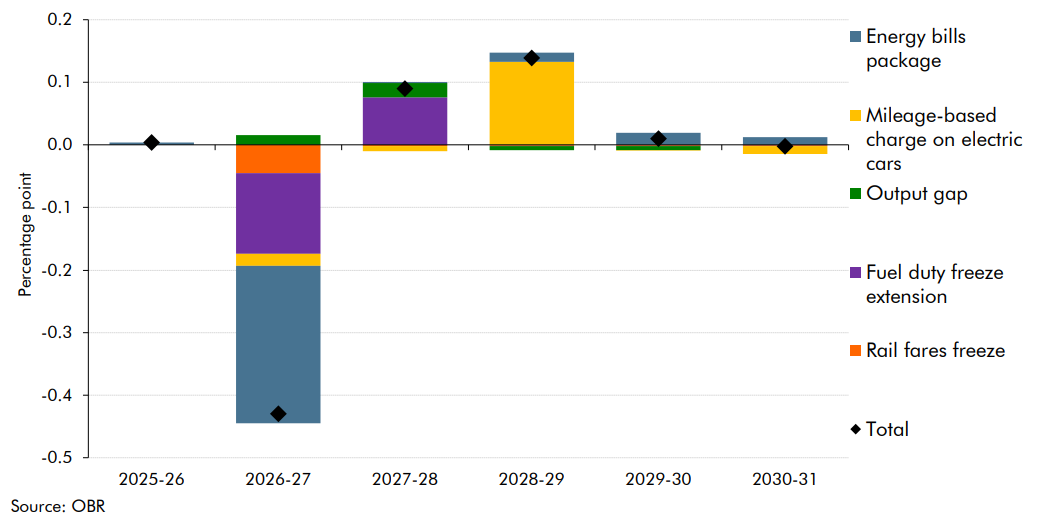

The impact of this Budget on interest rates is rather different to what was expected. An increase in borrowing over the next three years gives a small temporary lift to growth of 0.1% per year, although it leaves it unchanged by the end of the forecast. Meanwhile although this year’s Budget policies reduce the level of inflation by 0.4% points by 2026-27 – particularly through lower energy bills, the extension of the fuel duty freeze and freeze in rail fares – the OBR judges that these only partially offset higher-than-expected inflation – including from last year’s Budget measures, which added 0.5% points to inflation. It will be interesting to see what the Bank of England make of this. They’ll appreciate a lowering in the headline rate of inflation – even for temporary reasons – if it helps bring down inflation expectations. But looser fiscal policy against a constrained economy implies tighter monetary policy.

Policy impacts on real GDP and its components

Impact of Budget policies on CPI inflation

Business investment is set to decline as a share of the economy, according to the OBR, as a result of the relatively high cost of capital and low rates of return, alongside weak investment intentions and business confidence. Unemployment rises a little further amidst ongoing softness in hiring intentions. Earnings growth is expected to fall back to 3.3% in 2026 – similar to the Bank of England’s expectations – before falling back further to around 2.3% in later years. The further fallback in wage growth reflects a looser labour market, lower inflation and the impact from higher employer NICs. The OBR note that there have been sharper falls in the employment of the low paid than they expected, but isn’t sure whether that’s due to changes in direct employment costs or wider economic conditions. There’s no estimate of the impact from the Employment Rights Bill here either, as the OBR still feel they have insufficient detail.

The OBR highlights some key up and downside risks to the growth outlook. Notably they reference the proximity of US equity markets to dot.com bubble levels, and the risk of a global re-pricing of assets. Scenario analysis suggests a market correction would take 0.5-0.6% off UK GDP for a decline in UK equity prices of 15-35%. The rise in personal taxation in later years has the potential to lower output as well through disincentives to work. On planning reform, the OBR note that amendments to the Planning and Infrastructure Bill which may add new environmental safeguards and economic conditions pose downside risks through limiting the release of land for development. And further measures which reduce the returns to private landlords are judged likely to reduce the supply of rental property, risking a long-term rise in rents. But there’s an upside risk to growth from the UK’s new trade deals, particularly those with India and the EU. Meanwhile the impact of reforms to the non-dom regime has been in line with expectations so far, although the OBR flags that additional increases in the taxation of wealthy individuals could further incentivise migration.

Comparison of forecasts for key economic variables

Key takeaways for business leaders

With most of the tightening in fiscal policy once again postponed, and further policy support in the near-term, this Budget mildly improves the near-term growth outlook. The increase in benefit spending, while it delays needed action to ensure spending is affordable, will support consumer spending. Nonetheless, growth softens a little next year as fiscal policy still tightens. The outlook for interest rates is uncertain since the Budget includes measures to lower the rate of inflation, but also stimulates the economy in the near-term. On balance, markets continue to expect interest rates to bottom out around 3.5%, but there is more uncertainty than before. The labour market is expected to soften further, implying ongoing improvements in labour availability. The Budget did not contain material announcements on de-regulation and planning reform in particular, and these remain key policy priorities for the government. Meanwhile, the announcement after the Budget that unfair dismissal rights would come into effect after 6 months rather from day 1 is a welcome compromise, but one that leaves plenty of work left to balance the needs of workers and employers fairly in the Employment Rights Bill.

About the author

Anna Leach is a well-known UK economist, who appears regularly in the broadcast and business media. She has over 20 years of experience in a variety of macroeconomic and policy roles in business organisations and the civil service.

Prior to joining the IoD in 2024, Anna was Deputy Chief Economist at the Confederation of British Industry (CBI), where she was responsible for macroeconomic analysis, business surveys (economic, policy and commercial) and economic consulting.

Earlier in her career, Anna was a member of the Government Economic Service, where she undertook policy roles at the Department for Work and Pensions, looking at labour market issues, and in the HM Treasury economic analysis team. Anna has an MSc and a BSc from the University of Warwick, both in Economics.

Join a thriving community of skilled directors and leaders

Ask us about membership