Our view on the Spring Statement The detail

It was a refreshing change to have a fiscal event that delivered in line with expectations, in marked contrast with the one we had in October.

Having been told that she was set to miss her primary fiscal rule (that the current budget (day-to-day spending minus tax revenue) should be in balance or surplus by 2029-30) by £4.1 billion in 2029-30 rather than meet it with a margin of £9.9 billion, the Chancellor rose to the challenge and found the necessary £14 billion to get her back to where she was in October.

The Chancellor delivered stability and reassurance to financial markets, who were relieved to be told that they would be asked for a little shy of £300 billion in 2025-26, rather than the £310 billion they were expecting. For the rest of us, there was a mix of growth downgrades and upgrades, more defence spending, less welfare spending, departmental budget cuts and a bit more tax revenue from more HMRC compliance officers and stronger growth in future years.

One was left with the sense that this was an awful lot of work to deliver £14 billion, a relatively small amount of money in the context of the public finances – the cuts to current spending amount to 0.6% of total current spending in 2029-30. And with only a 54% chance that this will be the last time the Chancellor has to adjust her plans to meet her fiscal rules, the likelihood is we’ll be back to the drawing board for the Autumn Budget. So while the fiscal rules may be working for markets, they’re hardly leading to stability for government spending plans.

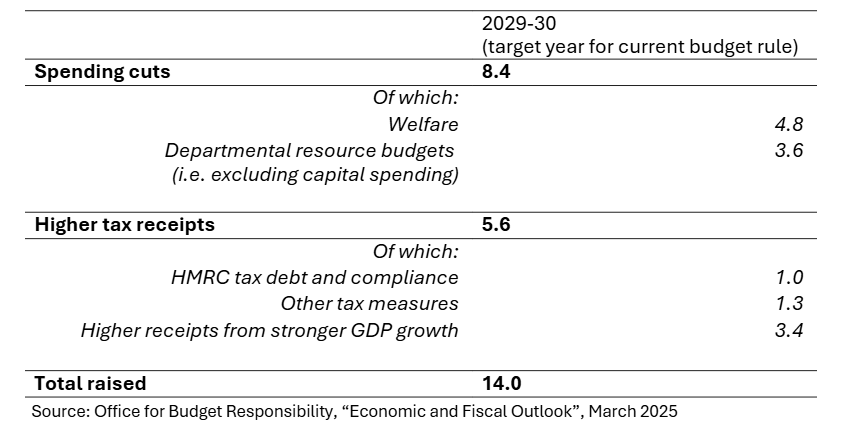

The £14 billion hole: what drove it and how’s it been plugged?

Before the impact of new policies, the Chancellor missed the first fiscal rule by £4 billion – a £14 billion deterioration. This mostly reflected higher debt interest costs from higher interest rates, gilt yields and inflation. Corporation and self-assessment tax receipts had also been weaker-than-expected, and this passes through into the forecast. The underlying drivers are the same ones driving the economic growth downgrade, but with a greater impact from movements in financial markets than from growth disappointments – understandable then that the Chancellor should place so much weight on the market response.

Here’s an overview of how the £14 billion gap has been filled:

A few points to note from this table. More of the hole is plugged from tax than you might expect, with the Chancellor benefitting particularly from the OBR’s judgement that planning reform pays off for GDP growth. On the departmental resource budget cuts, most of those arise from cuts to the International Development resource budget of £3.2 billion by 2029-30.

The growth outlook: down a bit, up a bit

Economic growth affects tax receipts and government spending – benefit payments increase with unemployment; in a growing economy, VAT receipts rise with consumer spending, corporation tax rises with profits, income tax receipts rise with incomes.

As expected, the OBR cut their growth forecast for 2025 to 1.0% from 2.0%. Their October forecast was always on the optimistic end: at the time that the OBR published, the average new independent forecast for the UK’s growth rate in 2025 was 1.2%. The independents have since come down to 1.0% – a rather smaller correction than the OBR has had to make. The OBR put their forecast correction down to higher uncertainty, higher interest rate expectations, higher gas prices and weaker productivity – productivity is the area in which the OBR has a tendency to optimism.

Planning reform gives growth a leg-up in future years. Growth every year in the period 2026-2029 is expected to be higher than the OBR predicted in October. Some of that is bounceback from weakness this year, but the role of government policy in supporting growth is highlighted, with 0.1% added to demand in the near-term from higher government spending, and 0.2% added by the end of the forecast horizon due to planning reform. Changes to the National Planning Policy Framework are judged to drive 170,000 of the expected 1.3 million cumulative net additions to the housing stock, affecting construction productivity and labour market efficiency (i.e. more homes for people to move in and out of supports better job matching). This helps increase tax receipts in future years.

Welfare reform so far gets the thumbs down when it comes to getting people off benefits and into work. The OBR have only been able to quantify the labour market impacts from one element of the welfare reforms: the decision to increase universal credit. And this reduces labour supply as it reduces incentives to work. Of course, the other actions within the welfare package are intended to push people towards work, but DWP have not yet been able to provide the OBR with sufficient evidence that this will be effective, and so the OBR will return to this in the Autumn. At which point they’ll also be in a position to assess the labour market impacts of the Employment Rights Bill – and there’s a gratifying reference to the Institute of Directors’ Policy Voice data on this on page 75 of the OBR report.

Public sector spending: is this austerity?

Overall, there’s little change to departmental budgets since October. Savings of 15% on back office functions total £2.2 billion to be delivered by 2029-30 – they’re hoping that much can be saved through voluntary redundancy and natural wastage. In the meantime, budgets have actually increased for much of the forecast period and have only been cut in the final two years – this reflects departments being compensated for the increase in employer NICs and a new transformation fund to support departments in finding productivity savings. The additional HMRC compliance officers will entail a larger settlement for that department. But the overall increase in budgets is more than wiped out by higher inflation, such that average real growth in departmental resource budgets is 1.2% from 2026-27 onwards – 0.1% points lower than in October. Most of the departmental budget cuts seem to fall on the International Development department.

If you’re a welfare recipient, this is a very tough package. The OBR notes that it’s the toughest since 2015, which included a four-year freeze to most working-age benefits and reductions to tax credits and universal credit. They also note that previous reforms have saved much less than initially expected, have taken longer to implement or have ultimately been unwound or cancelled.

Will this be enough?

Sadly, downside risks to economic growth remain pronounced, in addition to the challenge of delivering a highly ambitious and controversial package of welfare cuts, and the vulnerability to market movements in interest rates. The Chancellor’s margin for error remains the narrowest of slivers – a third of the average amount of fiscal headroom left by Chancellors since 2010.

The OBR highlight three risks which could bring the Chancellor back to the drawing board:

- Productivity weakness: If productivity doesn’t recover to its pre-pandemic trend, then output would be 3.2% lower and the current budget would be in deficit by 1.4%.

- Interest rates rising: A 0.6% point increase in Bank Rate and gilt yield expectations across the forecast would wipe out headroom.

- Global trade disputes: A 20% point rise in tariffs between the US and the rest of the world could reduce UK GDP by 1% at peak and wipe out headroom.

Gilt yields are already higher than the point at which the OBR locked them into their forecast, and we have the latest set of tariffs from the US – this time, on automotive. Odds are we’ll be doing this again in the Autumn.

About the author

Anna Leach is a well-known UK economist, who appears regularly in the broadcast and business media. She has over 20 years of experience in a variety of macroeconomic and policy roles in business organisations and the civil service.

Prior to joining the IoD in 2024, Anna was Deputy Chief Economist at the Confederation of British Industry (CBI), where she was responsible for macroeconomic analysis, business surveys (economic, policy and commercial) and economic consulting.

Earlier in her career, Anna was a member of the Government Economic Service, where she undertook policy roles at the Department for Work and Pensions, looking at labour market issues, and in the HM Treasury economic analysis team. Anna has an MSc and a BSc from the University of Warwick, both in Economics.

Join a thriving community of skilled directors and leaders

Ask us about membership