Enhancing UK Equity Capital Markets Competitiveness The Critical Issue of Share Buyback Execution Costs

As directors of UK-listed companies, it is imperative to address a significant challenge that affects the competitiveness of our equity capital markets and the returns of our shareholders: the high costs associated with share buyback executions.

This is for two core reasons. First shareholders are increasingly becoming litigious, if their interests are not being safeguarded then class actions are starting to follow which are quickly becoming significant time and risk sinks for boards. Second, the UK needs a healthy and competitive equity capital market to fund and support future growth. This article will delve into the current state of share buybacks in the UK, the frictional costs involved, and propose actionable steps to mitigate these issues, ultimately protecting the interests of our remaining shareholders.

The Prevalence of Share Buybacks in the UK

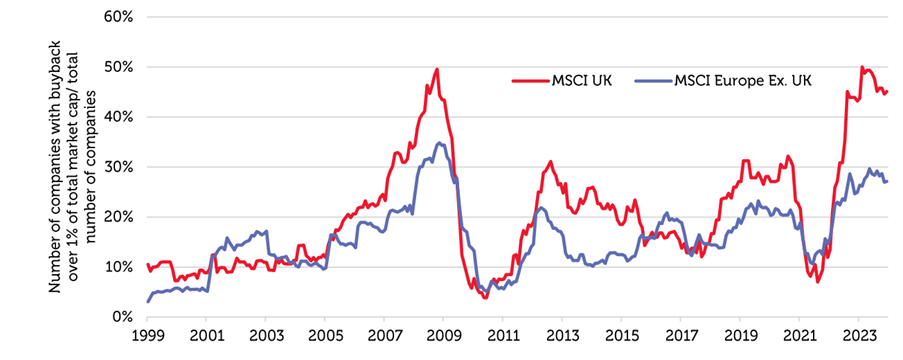

In 2024, UK-listed firms are expected to return approximately £120 billion to shareholders, with roughly half of this capital being distributed through share buybacks. This trend is particularly pronounced in the UK, where over 50% of companies in the MSCI UK index are anticipated to engage in share buybacks, the highest percentage globally. While share buybacks can be an effective way to return capital to shareholders, the execution costs in the UK are alarmingly high.

The Cost of Friction in Share Buybacks

The UK stands out as probably the most expensive market in the world for issuers to recycle capital via share buybacks. The frictional costs of executing these buybacks are estimated to be in the range of 6 to 8%, significantly higher than in the US, where such costs are around 3%.

This disparity can, in part, be explained by three factors, one of which a board can control for, and two that require UK regulatory revisions. When a board approves the allocation of capital to a share buyback, they can attach some parameters, which if designed well, will protect their remaining shareholders interests and hence protect the board itself.

Share buybacks consolidate share ownership to the remain shareholders. These shareholders’ interests, from the perspective of the implementation of a buyback, is that the execution is optimised to attempt to repurchase as many shares as possible. However, there are execution solutions, designed by banks equity derivatives desks, which sound fantastic but do not attempt to achieve this goal. This can result in both the execution risks and costs being substantially higher than they should have been and the programme becoming at risk of falling outside of the regulations safe harbour protections against insider trading and market abuse. One need to look no further than Oliver Shah’s Sunday Times article to see the problem.

Revising Disclosure Laws

The two factors that are outside of the direct control of the board relate to how and when buyback execution details are disclosed, and some of the execution constraints imposed on issuers when they repurchase their shares. The larger impact of these is due to the stringent disclosure requirements in the UK. Unlike in the US, where companies only need to disclose the board’s approval of a buyback and report any activity on a delayed basis, UK issuers must disclose detailed information about the buyback program before it begins and provide near-live updates on the execution. This transparency, while beneficial for market hygiene, drives up the share price before the issuer can purchase any shares, resulting in fewer shares being bought back and a reduced benefit for remaining shareholders. As mentioned in this FT OpEd, the UK regulators would be well served to consider allowing for long delays prior to publication of such data, like in the US.

Revisiting Safe Harbour Laws

Another critical area for improvement is the interpretation and application of safe harbour laws. Not only to bring scrutiny to the current practices which involve structured products, mentioned above, but to also to bring about revisions to the technical standards for share buyback executions. These were last revised in 2005, prior to the massive evolution in equity market structure and the proliferation of different types of equity trading venues. Updating these standards would provide more flexibility and better align with modern market conditions.

The Risk to Directors and Shareholders

The current state of share buyback execution in the UK poses significant risks to both directors and shareholders. Directors are at risk of class action suits if they fail to protect the interests of remaining shareholders. The high frictional costs and potential manipulation of share prices through flawed execution strategies can lead to legal challenges and damage to the company’s reputation.

For shareholders, the impact is direct: reduced returns on their investments. The capital returned via buybacks is material, especially when compared to the relatively small amount invested in new UK IPOs. Ensuring that this capital is returned efficiently is crucial for maintaining shareholder trust and attracting new investors, including UK pension funds.

Conclusion

Enhancing the competitiveness of the UK equity capital markets requires immediate attention to the issues surrounding share buyback execution costs. By delaying disclosure reports, revisiting and clarifying safe harbour laws, and updating the FCA’s conditions of trading, we can significantly reduce the frictional costs associated with share buybacks.

Directors must act swiftly to protect the interests of their remaining shareholders. The proposed changes are not only beneficial for shareholders but also essential for maintaining the integrity and competitiveness of the UK’s capital markets. It is our collective responsibility to ensure that our markets remain attractive to investors and that our shareholders receive the fair returns they deserve.

Addressing the high costs of share buyback executions is a critical step towards making the UK’s capital markets more competitive and ensuring that our companies remain match-fit for the future. By taking these steps, we can enhance investor returns, reduce legal risks, and maintain the UK’s position as a leading global financial hub.

About the author

Michael Seigne is a securities execution expert with over 30 years of experience in global financial markets. His career includes roles at leading investment banks, market-makers, and agency brokers, such as Managing Director at Goldman Sachs and Global Head of Execution Services at Redburn (Europe) Limited. In 2022, Michael founded Candor Partners Limited, a firm dedicated to enhancing outcomes for listed companies in share transactions, with a particular focus on optimising share buyback execution. His work aims to improve total shareholder returns through improvement of buyback execution strategies.

Join a thriving community of skilled directors and leaders

Ask us about membership