Director Weekly The Iran war has triggered the largest disruption to global oil supply on record. The consequences for the UK economy could be severe.

The scale of the disruption created by US and Israeli attacks on Iran is becoming clear. Yet extensive conversations with UK business leaders over the last two weeks suggest that many are yet to realise quite how bad things could get over the coming months.

The truth is that we are in uncharted waters. The International Energy Agency (IEA) says that the war has led to the largest supply disruption in the history of the global oil market. It’s twice as bad as the disruption created by Russia’s invasion of Ukraine; worse even than the 1973 oil embargo.

While the world is now less dependent on oil, the present interruption to supply is more extreme. Gas supplies are affected, too. The conflict is having a triple impact: on extraction, processing and distribution.

The resulting spike in energy prices will hit UK businesses hard if it persists. Early findings from ongoing IoD research suggests that about 1/3 of businesses are meaningfully hedged against gas and electricity price rises. Exposure levels will vary, and the most energy intensive businesses are likely to be those that are hedged (although those hedges may prove useless if force majeure applies). Yet the bottom line is that policymakers should be concerned about the impact of higher energy costs for business, who were already under pressure from rising tax and employment costs.

Businesses also face myriad cascading secondary effects. Haulage companies are levying surcharges; goods shipments are stuck in transit; suppliers’ prices are going up; financial decisions are being put on hold. Often, the only option right now is to wait and see what happens – which in itself is damaging to the economy.

Some companies may benefit from investments in supply chain resilience over recent years. Yet those only go so far. The blunt reality is that if critical supplies aren’t available, activity will grind to a halt. Planes can’t fly if airports run out of kerosene. Shell’s CEO warned this week<![if !supportNestedAnchors]><![endif]> that Europe could face fuel shortages by April.

The speed at which the outlook has changed is disorienting. Just a few weeks ago, we saw business confidence at its highest level since May 2025, enjoyed a welcome period of policy stability around the Spring Statement, and looked forward to inflation – and interest rates – easing downwards.

That has evaporated. Map the OBR’s worst-case scenario for a potential oil disruption onto today’s position and it suggests the UK could see inflation hit 8% next year.

The reality of these risks may not have yet have sunk in for many.

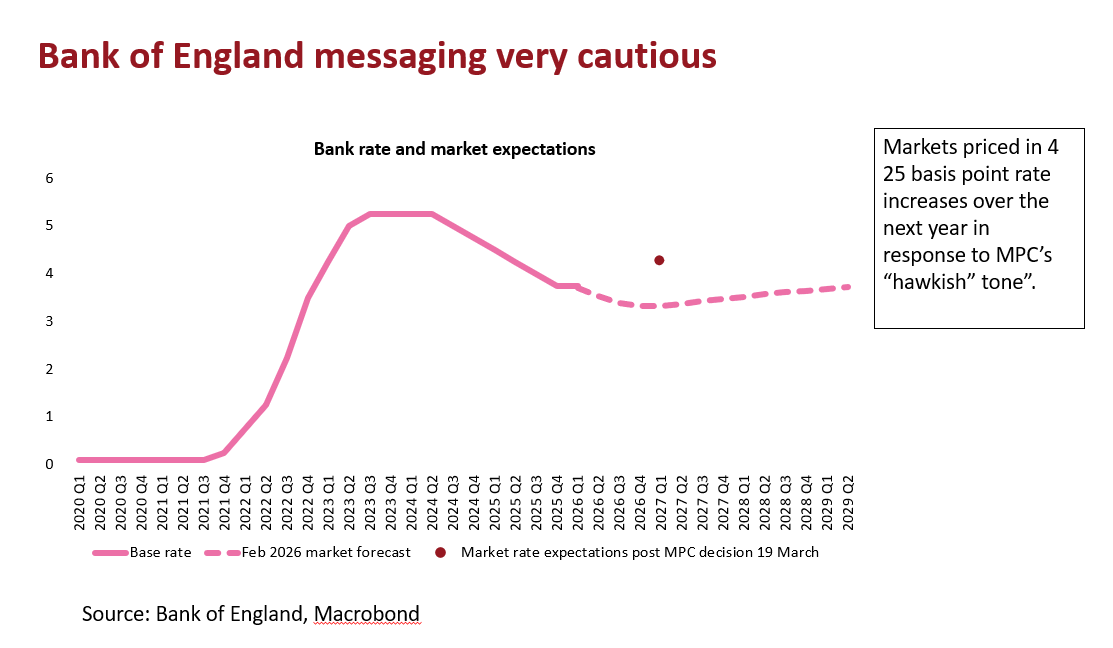

The Bank of England’s Monetary Policy Committee is already on the alert. It took a hawkish position in its 19th March decision, stating that it would “act as necessary” to keep inflation around the 2% target. Recent hopes of rate cuts have evaporated; the question now is when, and how fast, they start rising.

The big concern is that the economy starts from a much weaker position than in 2022. Growth has been mediocre, unemployment has been rising. An interest rate spike will heap further pain on the economy – so policymakers face an acute dilemma.

And unfortunately, there are no quick fixes. Even if the Strait of Hormuz reopened quickly, there would be a lasting impact on oil supply due to the damage already inflicted on infrastructure.

Fresh on the heels of the Ukraine war, we are once again facing a global hit to energy costs, which could have worrying consequences for the economy.

Read more here on why the conflict is a potential game-changer for inflation here.

About the author

Anna Leach is a well-known UK economist, who appears regularly in the broadcast and business media. She has over 20 years of experience in a variety of macroeconomic and policy roles in business organisations and the civil service.

Prior to joining the IoD in 2024, Anna was Deputy Chief Economist at the Confederation of British Industry (CBI), where she was responsible for macroeconomic analysis, business surveys (economic, policy and commercial) and economic consulting.

Earlier in her career, Anna was a member of the Government Economic Service, where she undertook policy roles at the Department for Work and Pensions, looking at labour market issues, and in the HM Treasury economic analysis team. Anna has an MSc and a BSc from the University of Warwick, both in Economics.

Director Magazine

This article is published as part of IoD Director, the authoritative voice of UK business leadership.

Get updates from Director

There has been an unexpected error.

Thank you for subscribing.

Unsubscribe at any time. Read our privacy policy.